| Crypto Words has moved! The project has migrated to a new domain. All future development will be at WORDS. | Go to WORDS |

Crypto Words is a monthly journal of Bitcoin commentary. For the uninitiated, getting up to speed on Bitcoin can seem daunting. Content is scattered across the internet, in some cases behind paywalls, and content has been lost forever. That’s why we made this journal, to preserve and further the understanding of Bitcoin.

Crypto Words is a monthly journal of Bitcoin commentary. For the uninitiated, getting up to speed on Bitcoin can seem daunting. Content is scattered across the internet, in some cases behind paywalls, and content has been lost forever. That’s why we made this journal, to preserve and further the understanding of Bitcoin.

Donate & Download the December 2019 Journal PDF

Remember, if you see something, say something. Send us your favorite Bitcoin commentary.

If you find this journal useful, consider supporting Crypto Words by making a donation buying us a beer.

Immutability as a Service

By Aleksander Svetski

Posted November 26, 2019

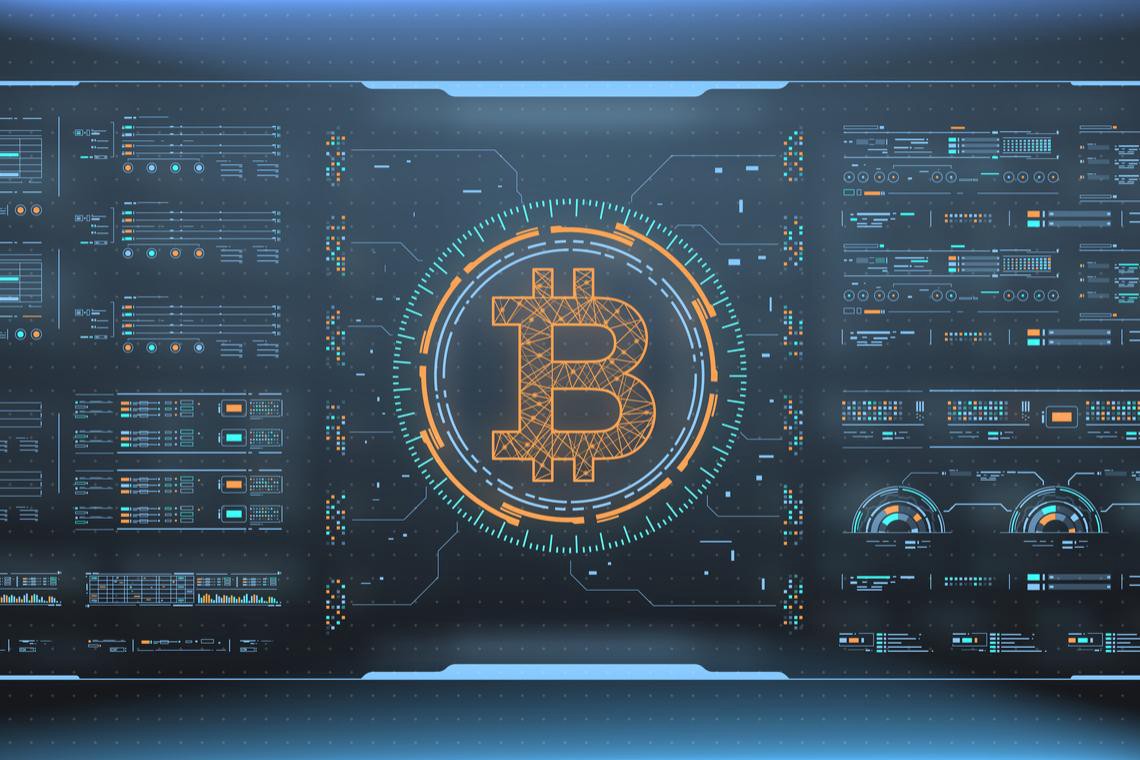

Bitcoin network = “IaaS” (not SaaS)

“Bitcoin provides immutability as a service”

There are not many applications in the world that need immutability, and perhaps only a couple that need to build immutability as part of their core stack. It’s just too expensive!

Now…If we view immutability as a service — one that any application in the world can “anchor” or connect to, then we begin to reframe how we view Bitcoin, i.e.; as a broader network that settles transactions or states with value associated to them.

An example here will help.

There is NO reason (or very little reason) that any company (tech or otherwise) today needs to buy, host and maintain its own server infrastructure. It’s costly and it makes up only a fraction of what matters in their actual business. So they use a cloud-based service such as AWS.

You’ll also note that because of the economies of scale; there are only three real options:

- AWS

- Azure

Why?

They got in early and they poured billions upon billions into it.

Immutability is similar (but also different).

Similar because the infrastructure required to make something truly digitally immutable is extraordinary (perhaps even more than all of the combined infrastructure that AMZN, MSFT and GOOG operate), and it only makes sense that people will anchor to it as and when they need to.

Different because it’s not something that can be run by one or a few parties. A concept like immutability (and things that inherently need it, i.e.; money) are only so if broadly owned. In other words; the more distributed and decentralized the architecture and higher the number the owners, validators and nodes, the more robust, costly and therefore immutable it is. Should one (or a few) entities manage all of it; it then undermines the value proposition and defeats the entire purpose.

The Immutable Network

Immutability as a service is what will bring more economic activity to the Bitcoin network in the long run, again; similar to the internet. The internet started off as a way to connect computers at a distance, and over time (as more people used and trusted it) it evolved into this new communication network that provides data / packet routing as a service. We built everything on top — and the innovation has been extraordinary.

The next step is baking monetary value into a protocol owned by the collective, whose core tenet is absolute digital immutability. A network where you can’t turn back time (like in the real world).

All of the economic value from applications that require this feature, along with any broader monetary / banking / capital or financial applications that require an absolute guarantee of the following key functions:

- Send

- Store

- Receive

Will accrue on it.

And as I’ve stated ad-nauseum, the more economic activity that occurs on and on top of the Bitcoin network, the more immutable and secure it will become. It’s compounding, it is self reinforcing, it has already hit a critical mass, and it’s now a runaway train.

Bitcoin is the autonomous digital network with the highest possible guarantee of the three core functions of money & finance.

Other consensus mechanisms

There are, and there will continue to be lots of other consensus mechanisms created. Some that might work; most that definitely won’t.

They may be used on their own networks, for applications that are either private, proprietary; or for applications that don’t require an absolute guarantee of immutability and security.

I personally don’t believe any money- related or high value applications will run on their own networks (except in vain over the next as this space evolves) because networks, especially those where the broad population participate, generally converge to unity.

It’s why we largely have one internet; one set of protocols for email; why we all use AC power; why, within a particular jurisdiction; the network of language converges to one, and similarly so with money (there is one USD in USA, likewise one AUD in AUS).

In fact — we see this as the world’s become more “global”.

English hit it’s critical mass, attained the primary network effect and it’s now more functional to speak English in most places around the world.

Aside from converging to unity due to efficiency and practicality, the world can probably only sustain ONE absolute, immutable, uncensorable, secure proof of work chain — because it’s expensive!

This chain is likely (at this stage at least) to be Bitcoin.

If we had to run proof of work for everything; we’d destroy the planet (plus it assumes nobody trusts each other for anything, which is a bigger problem anyway), and;

a) If someone wants to use it as a service; they’re going to go to the one that’s got the highest guarantee. That in itself will increase that network’s guarantee; leading to that self-reinforcing recursive effect I described earlier.

b) Furthermore; if you do have a novel, “light” consensus mechanism, that’s fast — you could in future anchor it to something like Bitcoin as and when you need to substantiate any claim or make a final judgement.

It’s this line of logic that leads me to believe most of the economic value will be swallowed up by the Bitcoin Network over the long term, not to mention the new concepts and innovations that will emerge using the ingredients of immutability and verification — like how facebook and instagram emerged from the internet.

In the next chapter, we’re going to explore the idea of Bitcoin as a new “Monetary Operating System”. Think of it like a computer operating system, eg; MacOS.

We can call it the BoS (very fitting).

Download the full guide at:

Debunking Bitcoin’s natural long-term power-law corridor of growth

By Marcel Burger

Posted November 30, 2019

Some models are useful, some fail to meet required underlying assumptions.

What’s this all about?

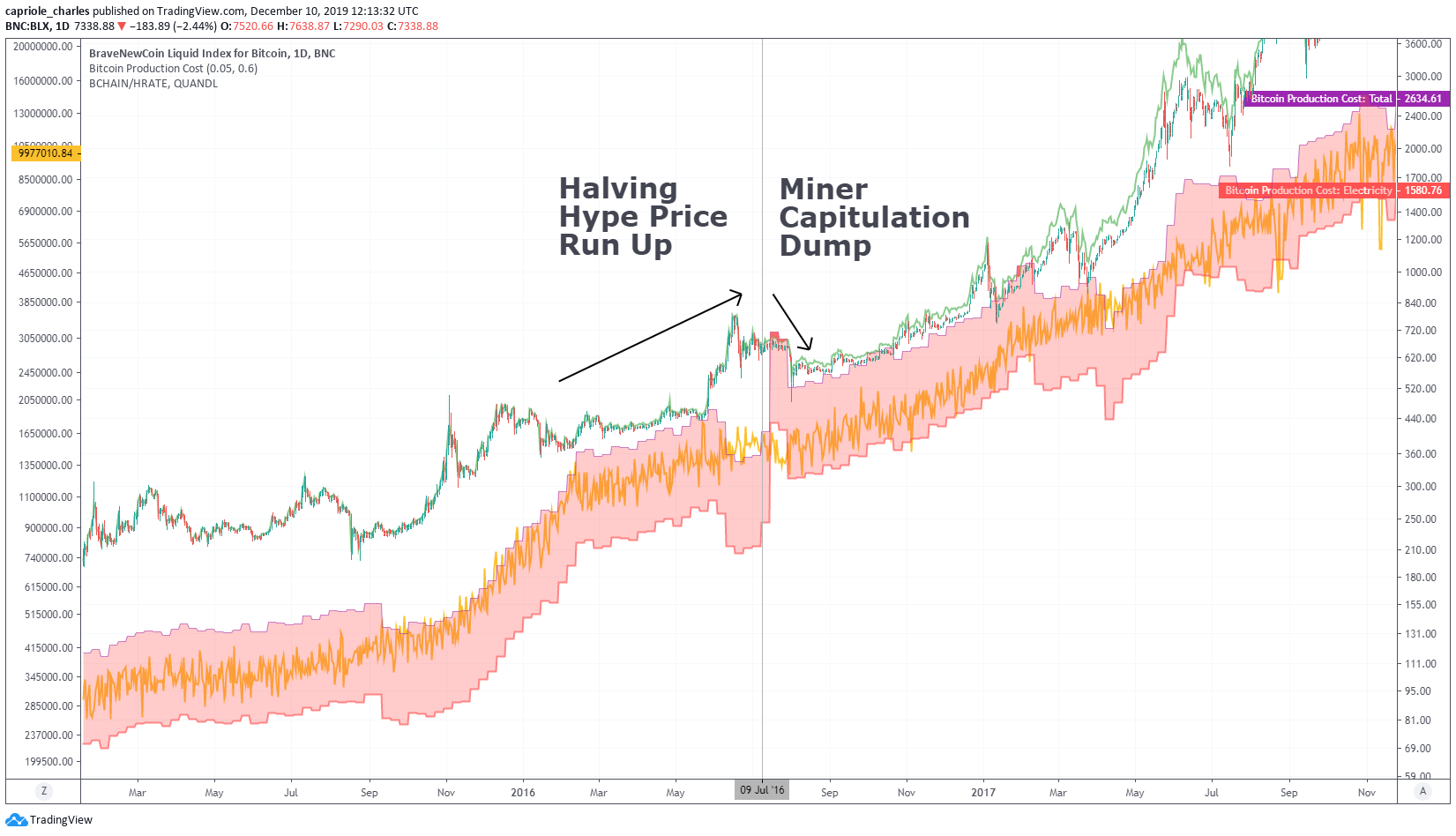

After PlanB wrote his (by now) famous piece on the relation between Bitcoin’s stock-to-flow ratio, a lot of people tried to debunk his model, including the author of this piece. It also inspired a lot of people to develop a competing model. But to my knowledge until today no-one succeeded in either a successful academically valid rejection of the model, or to come with a better model. One person in particular keeps coming back saying his model does a better job. Harold Christopher Burger’s idea was to build a comparable model, but instead of taking the natural logarithm of the stock to flow ratio as an independent variable, he thought the natural logarithm of time would be a better input. He reasoned that stock-to-flow is a function of time, so time itself must perform better. Even though Nick has demonstrated repeatedly (here for instance) how PlanB’s model is just better, Harold keeps claiming his work is superior. Time to take a closer look at his model and either applaud him for doing a fantastic job, or just send it (=his model) to the graveyard where it can take a rest with other failed attempts.

Regression again

Just like PlanB’s work, Harold’s work is also based on Ordinary Least Squares Regression. So, we check to see whether all the required assumptions are met. I have mentioned those assumptions as well in the first piece in which I reviewed PlanB’s model. Here they are listed once more.

(1) The expected value of the error term is zero (which means that on average the regression should be correct)

(2) The error and the independent variables should be independent.

(3) The error term should be homoskedastic (i.e. error terms have the same variance)

(4) There should be zero correlation between different error terms (i.e. autocorrelation is excluded)

After checking whether these hold, I’ll also take a look if cointegration applies here even though cointegration with time doesn’t make much sense. I’ll follow the same procedure as followed when reviewing PlanB’s work.

Data and Model

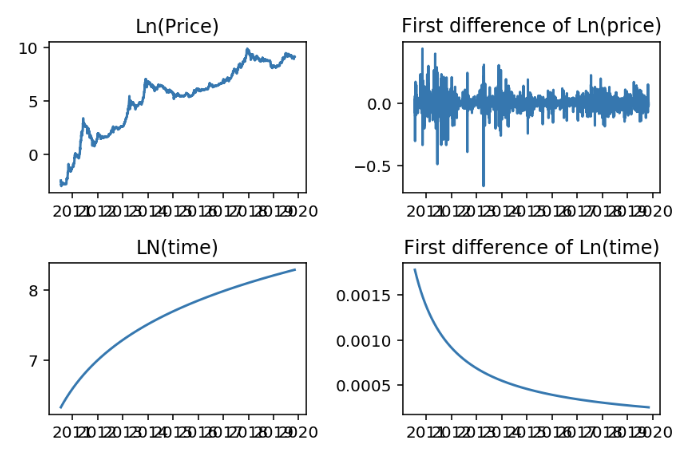

To build the model I used the CoinMetrics dataset which can be found here. All data before a price tag for bitcoin was known is discarded. The first day of the dataset is presented as day 1, the second day as day 2 and so on. So we’re counting the days as of day the first price tag is available. We take natural logarithms of both the price tags and the day counts. So our data starts like this:

Start of the dataset with time as days counted since start of the set

Start of the dataset with time as days counted since start of the set

or like this:

Start of the dataset with time as days counted since Jan 1st 1970 (UNIX)

Start of the dataset with time as days counted since Jan 1st 1970 (UNIX)

or like this:

Start of the dataset with time as days counted since bitcoin’s Genesis block (Jan 3rd 2009)

Start of the dataset with time as days counted since bitcoin’s Genesis block (Jan 3rd 2009)

Building the model and testing assumptions

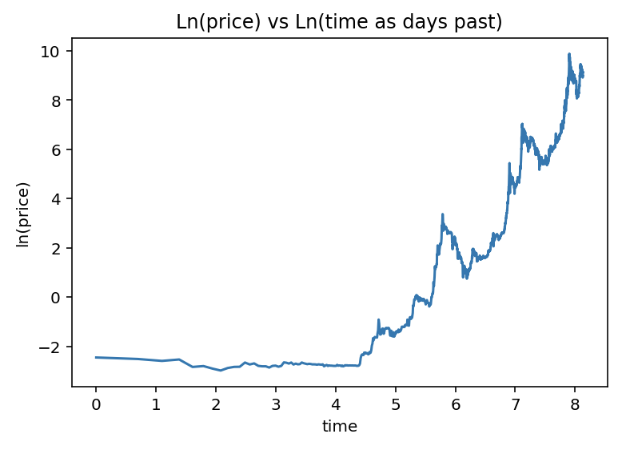

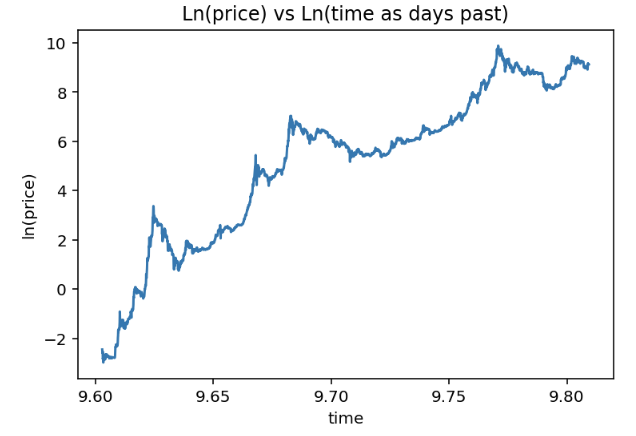

Before we start checking whether the assumptions hold up, we’ll start with some visual inspections of the data. Let’s see how the log-log chart looks like in case we work with time as days past since first measure. Time is a relative concept, so the performance of the model will be dependent of the point in time we consider as point 0.

Relation between ln time and ln price as time is days since first available price tag for bitcoin

Relation between ln time and ln price as time is days since first available price tag for bitcoin

Another logical starting point would be January 1st 1970 as day 1, we’ll go with that and look how the relation changes.

Relation between ln time and ln price as time is days since 1–1–1970

Relation between ln time and ln price as time is days since 1–1–1970

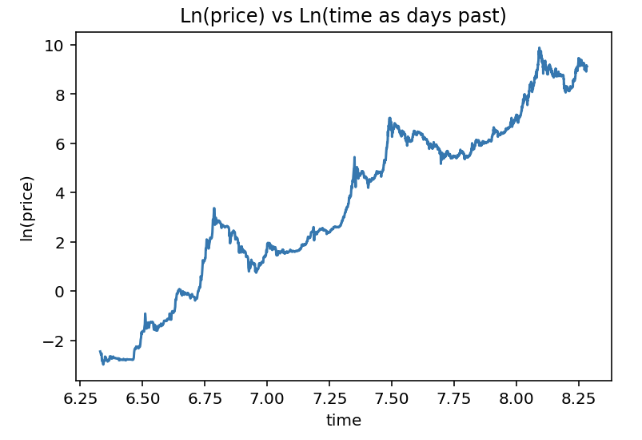

Relation between ln time and ln price as time is days since January 3rd 2009

Relation between ln time and ln price as time is days since January 3rd 2009

Starting to count the days as of the 3rd of Jan 2009 while first prices are not available seems a bit strange to me. It feels a bit like cherry picking the most suitable relative time series. This is what Harold used in his model, so we go with it as well here. Taking the first two would not return meaningful results as there would be too much non-linearity in those relations anyway. I would like to remark that this is where the model already starts to become shaky.

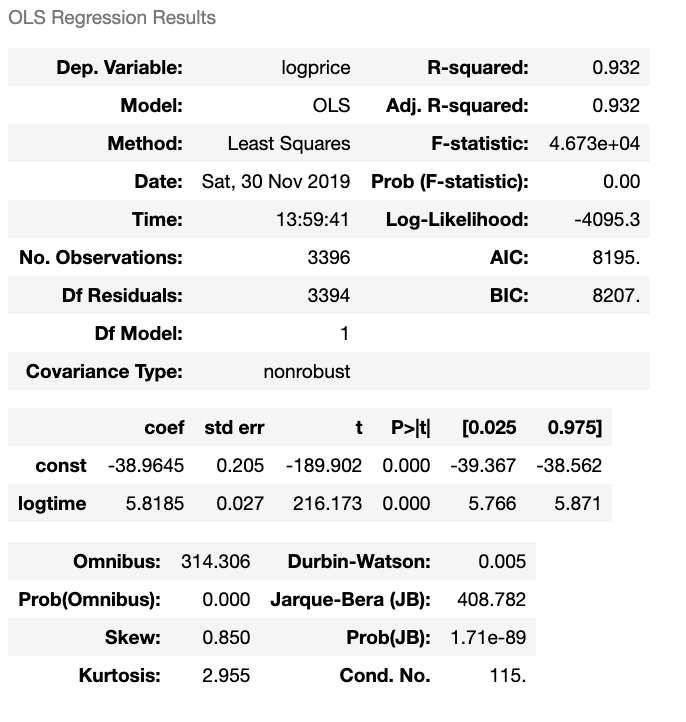

After running the regression, it’s time to take a closer look at the regression results and to research the model residuals. Here’s the regression result:

Regression results for ln time vs ln price

Regression results for ln time vs ln price

Even though R-squared is quite high, R-squared is not a very meaningful metric when we evaluate the regression of two non-stationary time series. It often turns out to be quite high when we’re using trending series and we should be aware of spurious regression. Further, the coefficients seem to be both significant, but the main question is whether the underlying model assumptions are met.

Residual analysis

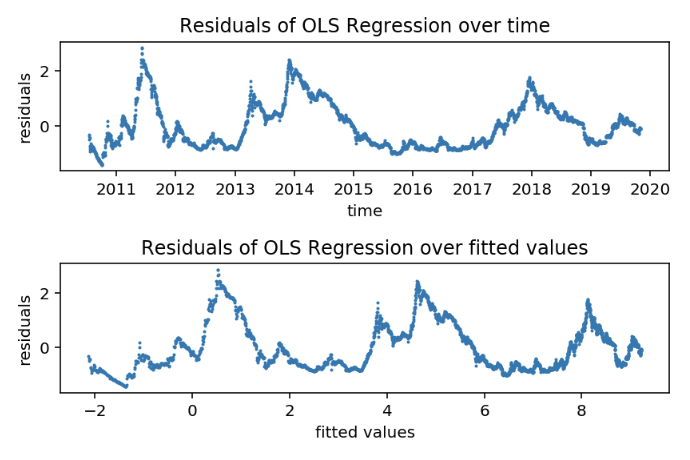

We’ll take a look at the residuals to check for possible issues with the model.

Plots of the residuals that follow from the regression

Plots of the residuals that follow from the regression

There’s a very clear pattern observable in both plots, which tells us that the residuals are likely to be autocorrelated, which would mean that the 4th assumption is not met. Next to that, we can also clearly see that the variance differs over time, which would indicate that the 3th assumption is violated as well. Both violations would lead to a falsification of the model.

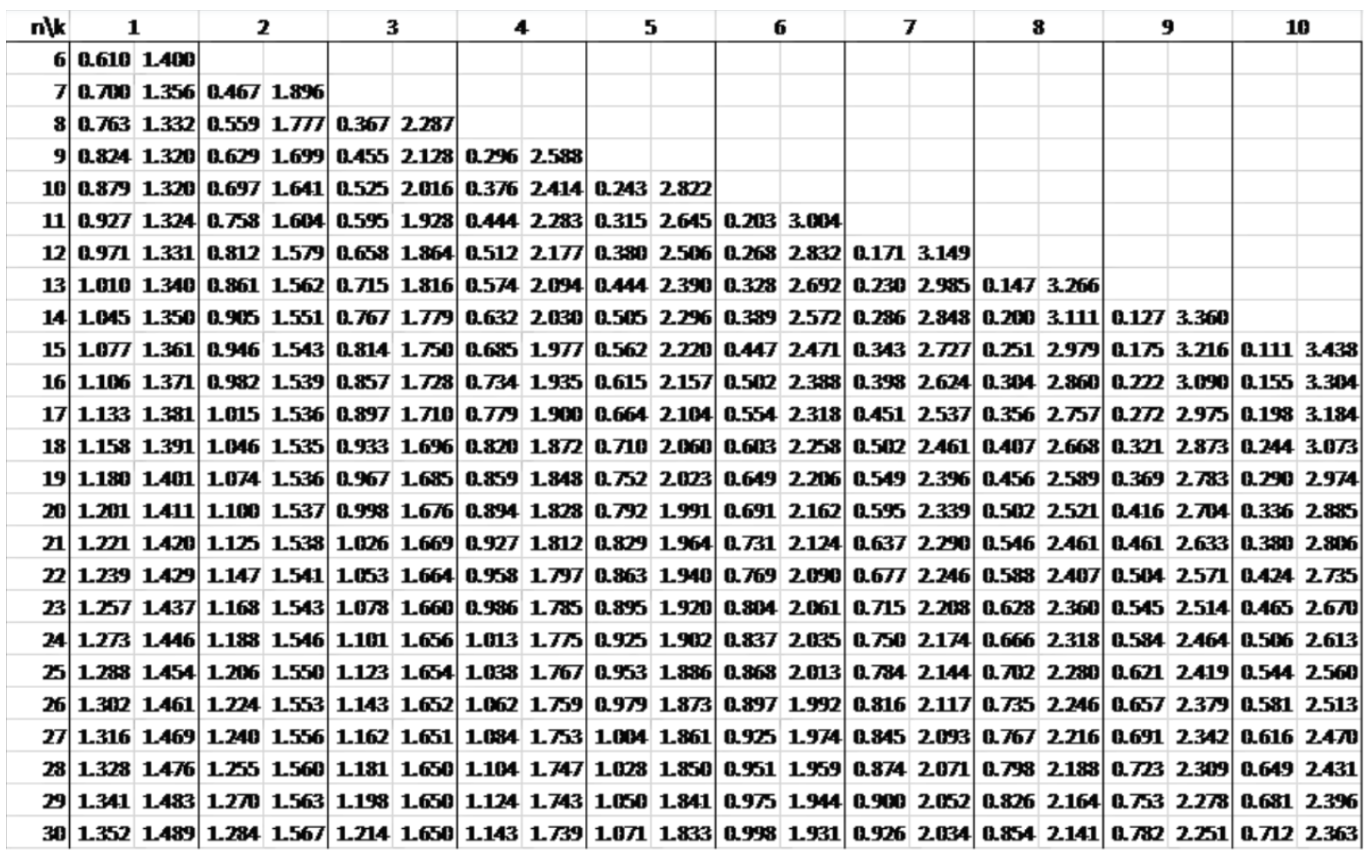

We will test for autocorrelation to make sure that this is an issue. The Durbin Watson statistic turns out to be 0.005 (check OLS results above) which is much smaller than the allowed lower bound value (see DW table in the Appendix).

Sofar, I would conclude the model’s fundamentals are no good, and the only reason to not reject it, would be in case we can show the variables are cointegrated.

Cointegration and Order of Integration

In order for two time series to be possibly cointegrated, those time series have to be integrated of the same order. Time to check how the both series are integrated, as they are both clearly non-stationary (both series trend up). Let’s have a look at the original series and their first differenced series. (Differencing means taking the difference of two consecutive values in the same time series.)

Variables over time and their first differenced series

Variables over time and their first differenced series

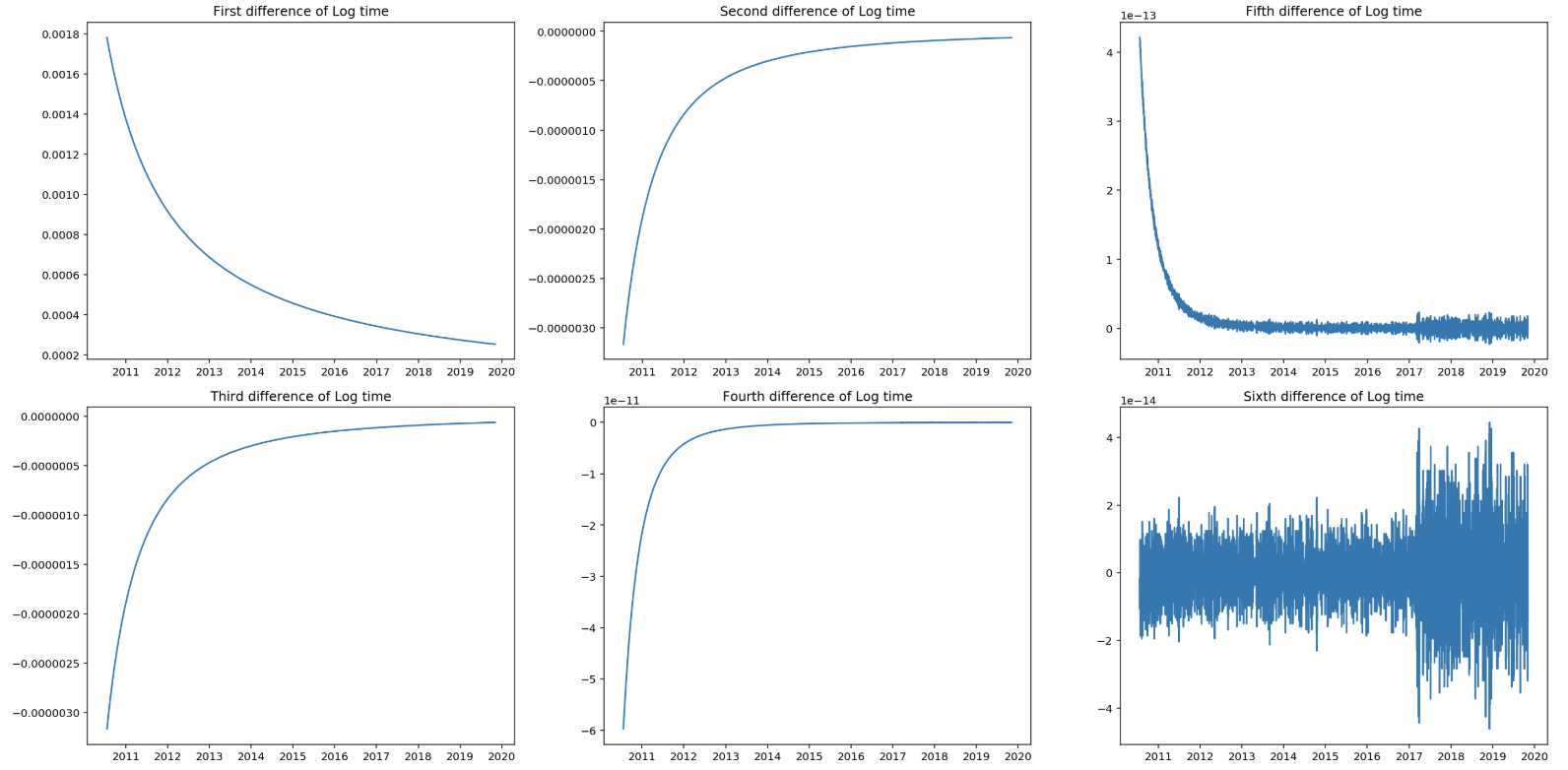

The charts above show that both time series are not stationary. Ln(price) is integrated of the first order as it shows to be stationary after differencing the series once. For log(time) we have to look further, as differencing once didn’t result in a stationary series. We keep on differencing to find the integration order for log(time), which resulted in the following:

Log(time) seems to be 6th order integrated.

Log(time) seems to be 6th order integrated.

Log(time) seems to be integrated of the 6ht order. This tells us that both variables are integrated of a different order and therefore cointegration is off the table. No need to run any further checks or statistical tests, as this requirement is not met.

EDIT: The 6th order integration as mentioned above is not proven by any test. In fact I learned that it even might not be reaching stationarity at all. The graph showing the sixth order difference, illustrates that we reach the limitations of the computer, as we witness floating point noise. For the conclusion it doesn’t matter. Special thanks to Hmatejx for pointing this out.

Conclusion

The model as developed by Harold Christopher Burger (more detail here: https://medium.com/coinmonks/bitcoins-natural-long-term-power-law-corridor-of-growth-649d0e9b3c94) is falsified. Since the model is falsified there is no need to compare it to any other model and PlanB’s stock to flow model in particular. A first threshold to compare a model to other models is that it should meet the fundamental assumptions.

Appendix

Durbin Watson table

References

- https://medium.com/@100trillionUSD/modeling-bitcoins-value-with-scarcity-91fa0fc03e25

- https://medium.com/coinmonks/bitcoins-natural-long-term-power-law-corridor-of-growth-649d0e9b3c94

- CoinMetrics Datasets, https://coinmetrics.io/data-downloads/

- M. Verbeek, A Guide To Modern Econometrics

- http://www.real-statistics.com/statistics-tables/durbin-watson-table/

Bitcoin Operating System

By Aleksander Svetski

Posted December 1, 2019

Bitcoin is a new “Monetary Network”, not a “Payments Technology”.

Bitcoin is the first time we’ve combined Money as a unit, with Money as a Network, into one thing.

And because it’s so different, it’s hard to wrap our heads around it.

The problem is further compounded by the fact that nobody really understands money, but most people get payments. Payments are easy: move money, and because it’s been handled digitally for the last 20–30yrs now, it’s even easier to grasp.

But money, that’s a much broader, more foundational concept, and to understand Bitcoin better; we’ll need to understand its real innovation, and in the process separate ‘money’ from ‘payments’.

As we’ve established, Immutability is derivative of cost. It’s this cost of validating transactions and maintaining the network of distributed but consistent ledgers that gives something like Bitcoin its immutability.

Bitcoin’s true innovation was an autonomous network that can establish the authenticity and validity of the state of the broadly distributed ledger.

The ONLY advantage of using this type of costly infrastructure is for actions that require a large degree of trust and assurance, those that should never fail and those that should not be easily reversed. There are a limited set of these, i.e. every transaction / or state change that happens in the world does NOT need this.

The world works pretty fine right now.

Could we make it better by stamping a “net state” to something immutable once a week / once a month?

Yes — definitely. But every transaction? No way. It’s just overkill.

Bitcoin is the most secure / immutable network that exists, NOT because of its “blockchain”, but because of its elaborate and expensive authentication mechanism. Your laptop has the ability to process hundreds of thousands of transactions a minute. That process is trivial. Payments is trivial.

Autonomous, distributed validation is the innovation.

And this is where people go astray.

People don’t ‘get’ bitcoin because they perceive it as some form of payments technology, or some “blockchain” mechanism (which they don’t really understand) for moving funny internet money (which they also don’t understand). That’s not what Bitcoin is.

Bitcoin is a complete reinvention of “money” — the world’s oldest social contract and society’s most foundational layer.

To understand its impact, you need to have a broad understanding of both networks and money. The problem is, most people don’t. In fact, nobody really understands what money is, because it’s not taught anywhere. Few can define it, whether they’re in banking, finance, technology, fintech, capital markets, and especially payments — so they apply their biases to it, and completely miss the point.

It’s like discussing the structure of the egyptian pyramids with your pet goldfish. The goldfish simply lacks the context.

Money requires an understanding of our evolution as a species, anthropology, biology, social engineering, psychology, game theory and what I like to call “the societal stack.” Discussing this is well outside the scope of this section, but I’ll touch on an area which I hope will give you a reference point, the societal stack, in a subsequent section of this edition of The Bitcoin Times.

The complexity of network dynamics doesn’t make the job of understanding Bitcoin any easier. I will touch on this further in a dedicated section — but suffice it to say networks are just as foreign to our intuitive understanding of the world as the pyramids are to the goldfish — the track record of the experts adds weight to this.

Back to payments VS money.

Bitcoin is not a “payments technology”. It’s fundamentally a reinvention if money. Like the motor vehicle was a reinvention of transport — not a better horse and cart. Same as the internet. It reinvented the fabric upon which we communicate. It reinvented the way information is transported. It did not push more, richer or smarter “data” through the phone networks infrastructure.

It used that infrastructure as physical onramps; but the internet is not the cables, or the hardware — it’s so much larger.

That’s why it swallowed them up and is the foundation upon which the majority of today’s society operates. And what’s more, the internet is only picking up speed. Bitcoin is where the internet was in the late 80s. Still largely misunderstood. People are still arguing about speed of payments! They don’t realise that “payments” as we know them today will completely transform.

The same way we’re no longer talking about the quality of the phone call and number of phone calls this “internet thing” will support, we will see new conversations emerge for what can be done on Bitcoin.

The world is changing. The internet was only the beginning….Bitcoin is the next chapter.

Speaking of next chapters, as we near the end of the Medium series for the first edition of The Bitcoin Times, we’re going to begin exploring networks, how the function and dig into where there are some high level conceptual similarities to the internet.

Download the full guide at:

Could Bitcoin’s privacy benefit from Litecoin’s EB MimbleWimble proposal?

By Pieter Wuille

Posted December 2, 2019

It’s not that simple.

I would personally very much like to see Confidential Transactions in Bitcoin. Hiding transaction amounts by default - while not a silver bullet for privacy on its own - would make CoinJoin a lot more powerful (right now you need to use matching amounts because you’d leak linkage otherwise anyway). I think it’s fair to say that it may help achieve a level of privacy that is very hard to reach with existing on-chain techniques.

Confidential Transactions however very fundamentally change how transactions work, as cleartext amounts are currently expected in transactions. Without (extremely invasive) hard fork, this cannot be changed. Even if they’re suddenly permitted, nobody can force existing wallets to suddenly adopt them. Doing so would break compatibility, and go against very basic expectations of not invalidating existing non-broadcast transactions. Such a change being successful probably implies Bitcoin lost some of its most valuable properties to begin with. Thus: CT (or any form of amount hiding) has to be opt-in.

But opt-in doesn’t need to imply opt-in on a per-transaction basis. An extension block effectively does that: by having two clearly delineated sides and a need for explicit, possibly slow/expensive, operations to transfer between them, you create a world where CT is the default, and possibly even cheaper than the other side. Sure, people still have the option to use the legacy side, and for a long time they probably will due to compatibility reasons, but in the long term it probably means much better privacy than any solution with per-transaction choice for CT or not. It turns out that CT-in-an-EB is also far simpler and more efficient than trying to hack it into the existing transaction structure.

So, I believe that Extension Blocks are the only (somewhat) practical way of introducing CT to Bitcoin.

That said, there are many caveats:

- CT transactions are far more computationally expensive and larger than current transactions, and it would be very unfortunate if the more private choice ends up being more expensive to use.

- CT introduces a much stronger assumption on cryptography than we currently have. You can’t just run through the UTXO set, sum up the values, and see that it doesn’t exceed the expected subsidy.

- In fact, CT inherently either must make privacy condition on cryptographic assumptions, or soundness (=printing of money). Bitcoin currently relies on the ECDLP assumption for theft, but this can (in the long term) be upgraded to another assumption if necessary (e.g. because we believe ECDLP is on shaky grounds, quantum computing, …). With CT this is not so easy anymore, as this assumption will now cover amounts as well.

- It’s a pretty damn big change that would need a huge demand from the ecosystem to be successful.

- All the same issues apply to MW, and more. MW is a more advanced form of CT that has an even more invasive impact on basic data structures, and probably simply cannot be done without an EB at all, as it is so fundamentally different from Bitcoin’s current blockchain (the MW blockchain can shrink over time!). It also removes Script or even the ability to have something Script-like.

Let me come back to point (3) above. There is a very fundamental result in zero-knowledge proof techniques that you cannot have both unconditional privacy and unconditional soundness. We however do know of ways to have either unconditional privacy or unconditional soundness, so there is a design choice between them.

- CT with unconditional privacy but computational soundness is the most common choice. This means that if somehow ECDLP breaks (math breakthrough, unexpected structure in secp256k1, quantum computer), someone could undetectably print coins, but the privacy of past (and future) transactions would be unaffected. To the best of my knowledge, Monero, ZCash, Grin, all use this model.

- CT with unconditional soundness but computational privacy is also possible. This means that an ECDLP break would not let anyone print coins, but the privacy of future (and past) transactions would be at risk. Unfortunately, this choice is much less efficient, and pretty much no systems use it.

Given Bitcoin’s design focus on controlled inflation, I expect that many people would prefer the second model over the first if a choice needs to be made. There is however also a point to be made that if ECDLP is broken, the future of the system is inherently at risk, but we may not want to give up the privacy of the past when that happens - a point in favor of the first model.

The nice (or scary…) thing about an Extension Block based CT design is that we could have either, or both, and without actually directly affecting the value of the legacy chain. You’d need to move coins explicitly to the CT side, and if unexpected inflation would happen there, simply not all of it would be able to move back to the legacy side. Unexpectedly, this may actually mean a different exchange rate for coins on both sides, if the public’s trust in the security for one is seriously affected.

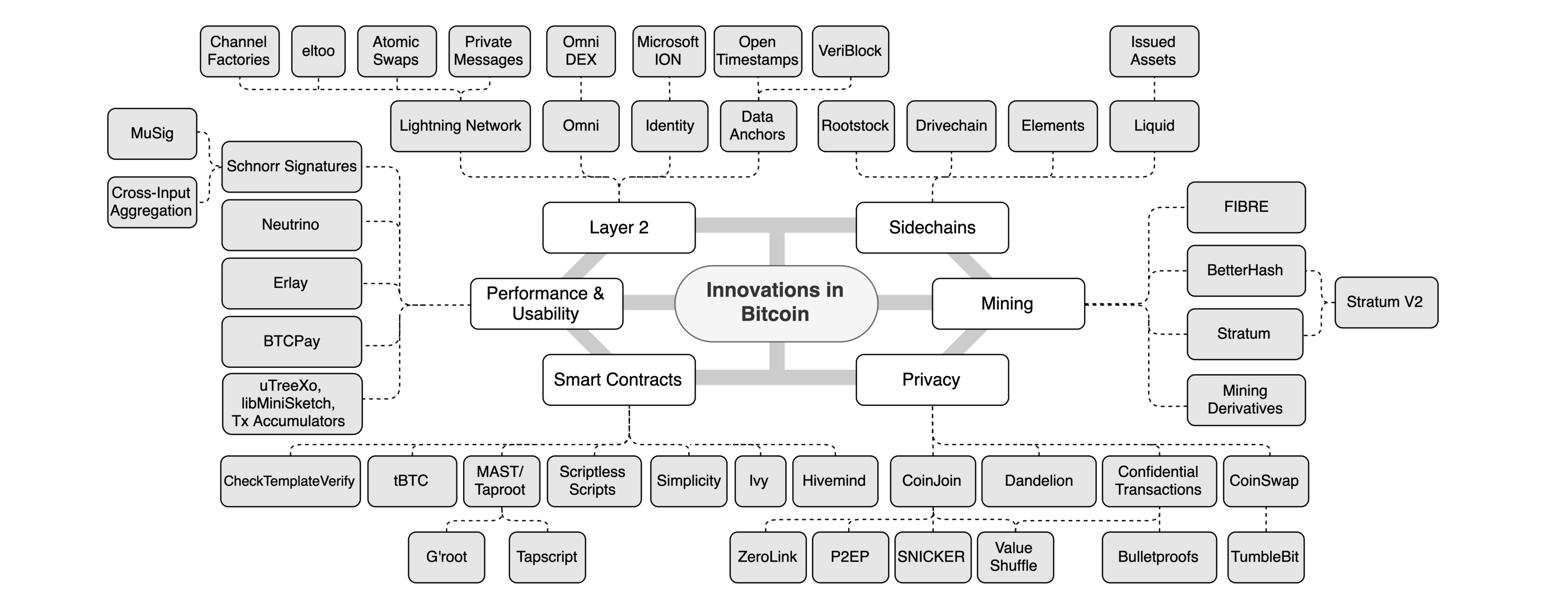

A Look at Innovation in Bitcoin’s Technology Stack

By Lucas Nuzzi

Posted December 3, 2019

Bitcoin has come a long way over the past ten years. Relative to the first iteration of its software, the quality and reliability of current implementations has remarkably improved. Rapidly and organically, Bitcoin was able to lure a legion of developers to dedicate thousands of hours to improve, and at times revamp, most of its underlying codebase.

Nevertheless, Bitcoin is still the same. Much like a constitution, the core set of consensus rules that define its monetary properties, such as its algorithmic inflation and hard-coded supply, remain unchanged. Time and time again, factions have attempted to change these core properties, but all hostile takeovers thus far have failed. It’s often a painful process, but one that highlights and solidifies two of Bitcoin’s biggest virtues:

- No single party can dictate how Bitcoin evolves

- The lack of centralized control protects Bitcoin’s monetary properties

Interestingly, these are the rules that attract cypherpunks and institutional investors alike. These are the rules that make bitcoin an unprecedented type of money. However, these are also the rules that make developing software atop Bitcoin more challenging than any other digital asset. In essence, Bitcoin’s constitution awards developers a limited toolkit so that they can’t infringe upon its monetary policy. There’s too much at stake to move fast and break things.

That means innovation in Bitcoin requires creativity, patience, and perhaps most importantly, ego-minimization. After all, the fundamental rules embedded in Bitcoin’s constitution ultimately supersede technology. This is why Silicon Valley has had a hard time understanding Bitcoin’s value proposition, it’s not just a technology, financial instrument, or consumer application; it’s an entire monetary system supported by technology. Changing Bitcoin’s constitution requires a quasi-political process that can infringe upon its monetary properties, therefore, technological innovation is implemented as modules.

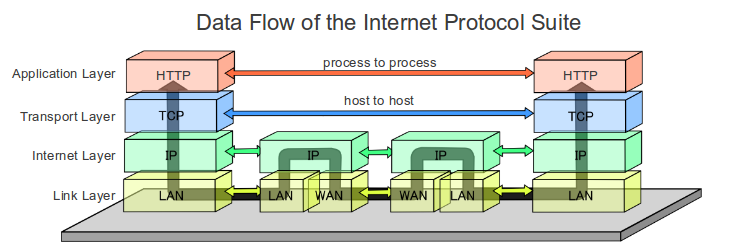

As often pointed out, Bitcoin’s modular approach to innovation is analogous to the evolution of the Internet’s protocol suite, whereby layers of different protocols specialized in specific functions. Emails were handled by SMTP, files by FTP, web pages by HTTP, user addressing by IP and packet routing by TCP. Over the years, each of these protocols evolved to provide the full experience you’re having this very second.

In Spencer Bogart’s excellent post on the emerging Bitcoin technology stack, he makes the case that we are now witnessing the beginning of Bitcoin’s own protocol suite. As it turned out, the inflexibility of Bitcoin’s core layer gave birth to several additional protocols that specialize in various applications, like Lightning’s BOLT standard for payment channels. Innovation is both vibrant and (relatively) safe, as this modular approach minimizes systemic monetary risks.

So much is happening at the many layers of Bitcoin’s technology stack, it can be incredibly difficult to keep track of emerging solutions. The diagram below is an attempt to map all relatively new initiatives and showcase a more complete picture of Bitcoin’s technology stack. It is not exhaustive, and it does not signal any endorsement for specific initiatives. It is, nevertheless, impressive to see that innovation is being pushed on all fronts; from layer 2 technologies, to emerging smart contract solutions:

Layer 2

There has been a lot of talk lately about the rate of adoption of the Lightning Network; Bitcoin’s most prominent layer 2 technology. Critics often point at an apparent decline in the number of channels and total BTC locked in Lightning; two metrics frequently used to evaluate user adoption. Although the community has converged on such metrics, it is important to point out that they are fundamentally flawed given the way Lightning works under the hood.

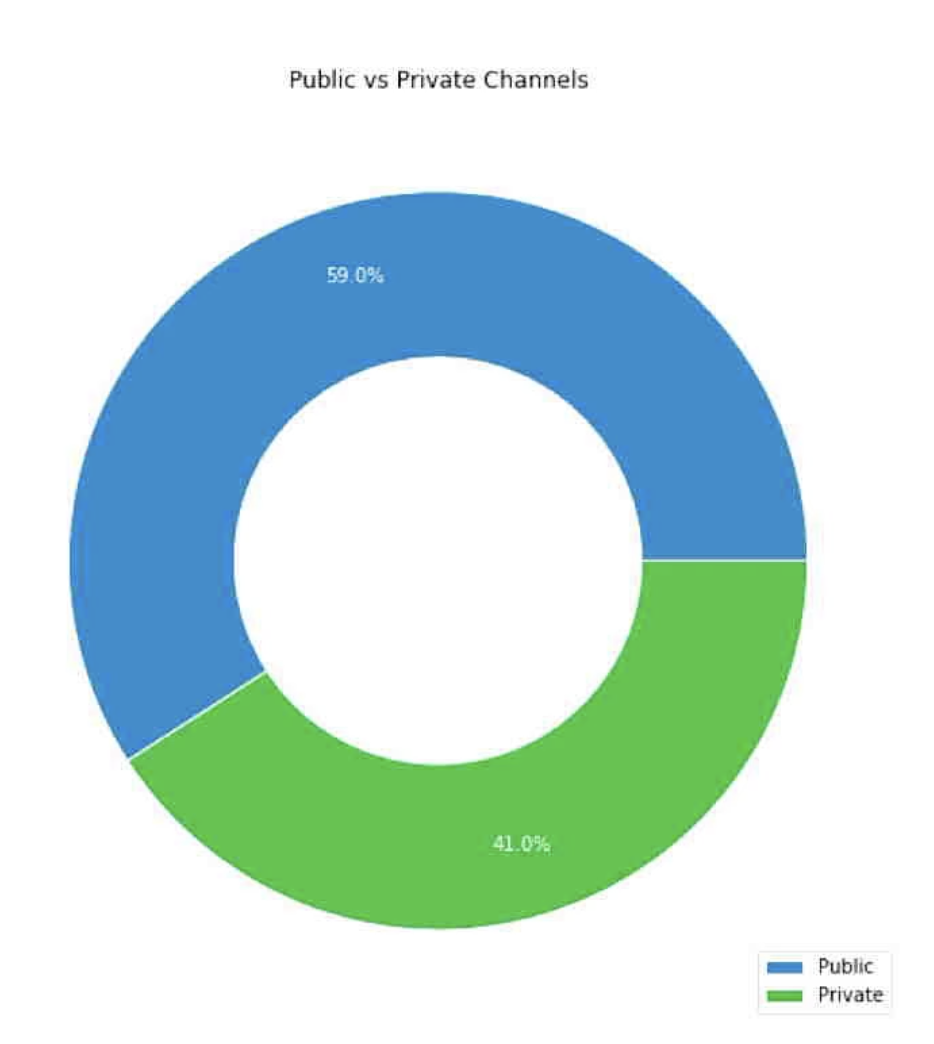

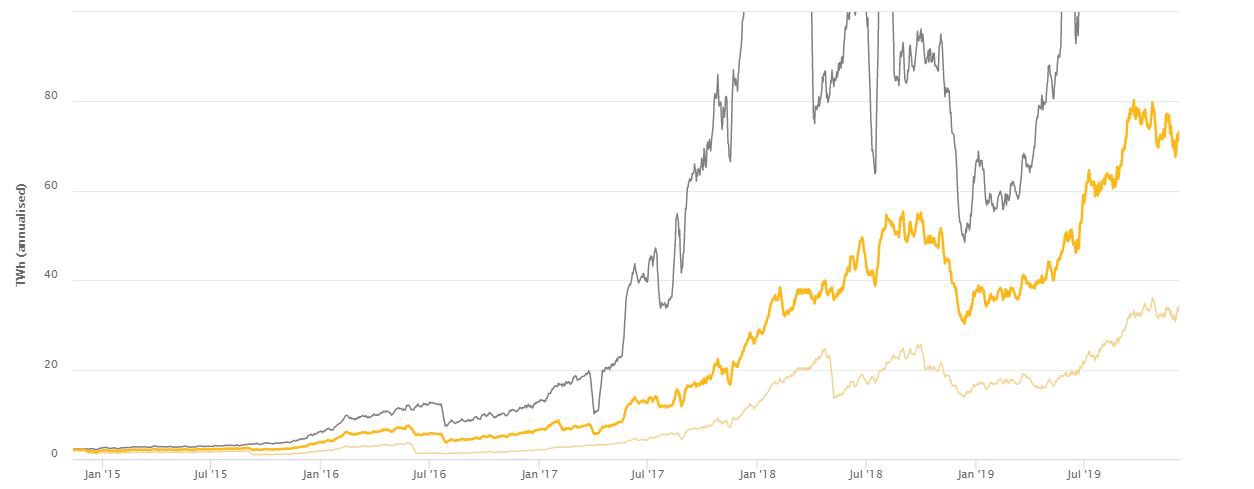

One of the most underrated virtues of the Lightning Network is its straightforward privacy properties. Since Lightning does not rely on global validation of all state changes (i.e. its own blockchain), users can transact privately over using additional techniques and network overlays, like Tor. At this point, we can estimate the percentage of private usage of the Lightning network by analyzing the number of channel opening transactions on-chain, and comparing that to the number of public channels off-chain. Christian Decker estimates that 41% of Lightning channels are private:

Activity happening within these channels is not captured by popular Lightning explorers. As such, an increase in private usage of Lightning results in a decrease in what can be publicly measured, leading observers to erroneously conclude that adoption is down. While it is true that Lightning must overcome substantial usability barriers before it can enjoy wide adoption, we must stop using misleading metrics to make assertions about the current state of the network. As Decker pointed out in his talk at the latest Lightning Conference in Berlin, even the above estimate of private vs. public channels is flawed, as the adoption of Schnorr signatures will make channel-opening transactions indistinguishable from regular transactions.

Another interesting recent development in the field of layer 2 privacy was the creation of WhatSat, a private messaging system atop Lightning. This project is a modification of the Lightning deamon which allows for relayers of private messages (the messengers that connect the entities communicating) to be compensated for their services via micropayments. This decentralized, censorship-and-spam-resistant chat was enabled by innovations in LND itself, such as recent improvements in the lightning-onion, Lightning’s own onion routing protocol.

The growth of Lapps, or Lightning Applications, demonstrate the wide applicability of these innovations when it comes to consumer applications, from a Lightning-powered cloud computing VPS to an image hosting service that shares ad revenue via microtransactions. And that’s just layer 2 innovation within Lightning. More generally, we define Layer 2 as a suite of applications that use Bitcoin’s base layer as a court where exogenous events are reconciled and disputes are settled. As such, the theme of data anchoring on Bitcoin’s blockchain is much broader, with companies like Microsoft pioneering a decentralized ID system atop Bitcoin. Such initiatives increase the demand for on-chain reconciliation and are instrumental for the long-term development of a Bitcoin fee market.

Smart Contracts

There are also a number of projects attempting to bring back expressive smart contract functionality to Bitcoin in a safe and responsible way. This is a significant development, because starting in 2010, several of the original Bitcoin opcodes (the operations that determine what Bitcoin is able to compute) were removed from the protocol. This came after a series of terrifying bugs were unveiled, which led Satoshi himself to disable some of the functionality of Script, Bitcoin’s programming language.

Over the years, it became crystal clear that there are non-trivial security risks that accompany highly-expressive smart contract functionality. The common rule of thumb is that the more functionality is introduced to a virtual machine (the collective verification mechanism that processes opcodes), the more unpredictable its programs will be. More recently, however, we have seen new approaches to smart contract architecture in Bitcoin that can minimize unpredictability, but also provide vast functionality.

The devise of a new approach to Bitcoin smart contracts called Merkleized Abstract Syntax Trees (MAST) has ignited a new wave of supporting technologies that attempt to optimize the trade-offs between security and functionality. Most prominently is Taproot, an elegant implementation of the MAST structure that enables an entire application to be expressed as a Merkle Tree, whereby each branch of the tree represents a different execution outcome. Along with Taproot will come a programming language called Tapscript, which can be used to more easily express the spend conditions associated with each branch of the Merkle Tree.

Another interesting innovation that has recently resurfaced is a new architecture for the implementation of covenants, or spend conditions, on Bitcoin transactions. Originally proposed as a thought experiment by Greg Maxwell back in 2013, covenants are an approach to limit the way balances can be spent, even as their custody changes. Although the idea has existed for nearly seven years, covenants were impractical to be implemented before the advent of Taproot. Now, a new opcode called OP_CHECKTEMPLATEVERIFY (formerly known as OP_SECURETHEBAG) is leveraging this new technology to potentially enable covenants to be safely implemented in Bitcoin.

At first glance, covenants are incredibly useful in the context of lending (and perhaps bitcoin-based derivatives) as they enable the creation of policies like clawbacks to be attached to specific BTC balances. But their potential impact on the usability of Bitcoin goes vastly beyond lending. Covenants can allow for the implementation of things like Bitcoin Vaults, which, in the context of custody, provide the equivalent of a second private key that allows a party that has been hacked to “freeze” stolen funds. There are so many other applications of this technology, like Non-Interactive Payment Channels, Congestion Controlled Transactions, CoinJoins, it truly deserves a standalone post. For more on this, check out Jeremy Rubin’s BIP draft.

It is important to note that Schnorr signatures are the technological primitive that make all of these new approaches to smart contracts possible. After Schnorr activates, even edgier techniques being can be theorized, such as Scriptless Scripts, which could enable fully private and scalable Bitcoin smart contracts to be represented as digital signatures (as opposed to opcodes). Similarly, Discreet Log Contracts also employ the idea of representing a smart contract’s execution outcome as a digital signature for better privacy and scalability. Together, these new approaches may enable novel smart contract applications to be built atop Bitcoin and Schnorr is the basis of it.

Mining

There have also been some interesting developments in mining protocols, especially those used by mining pool constituents. Even though the issue of centralization in Bitcoin mining is often wildly exaggerated, it is true that there are power structures retained by mining pool operators that can be further decentralized. Namely, pool operators can decide which transactions will be mined by all pool constituents, which grants them considerable power. Over time, some operators have abused this power by censoring transactions, mining empty blocks and reallocating hashing output to other networks without the authorization of constituents.

Thankfully, there are technologies that are attempting to flip that power structure upside down. One of the most substantial changes coming to Bitcoin mining is the second version of Stratum, the most popular protocol used in mining pools. Stratum V2 is a complete overhaul that implements BetterHash, a secondary protocol that enables mining pool constituents to decide the composition of the block they will mine and not the other way around. Stratum V2 also implements several optimizations, and allows mining pool constituents to better communicate and coordinate.

Another interesting development in the mining industry that should contribute to more stability is reignited interest in hashrate and difficulty derivatives. These can be particularly useful for mining operations that wish to hedge against hashrate fluctuations and difficulty readjustments. While these derivatives have yet to be productized, this marks an interesting evolution in the industrialization of Bitcoin mining.

Privacy

After our report on Schnorr signatures, some privacy-coin advocates were outraged by the suggestion that sufficient privacy may be optionally achieved in Bitcoin at some point. Although this suggestion may challenge theses around the long-term value proposition of privacy assets, there are a host of emerging protocols that can bring better privacy into Bitcoin. Although it is likely that privacy in Bitcoin will continue to be more of an art than a science, there have been interesting innovations on this front that are worth highlighting.

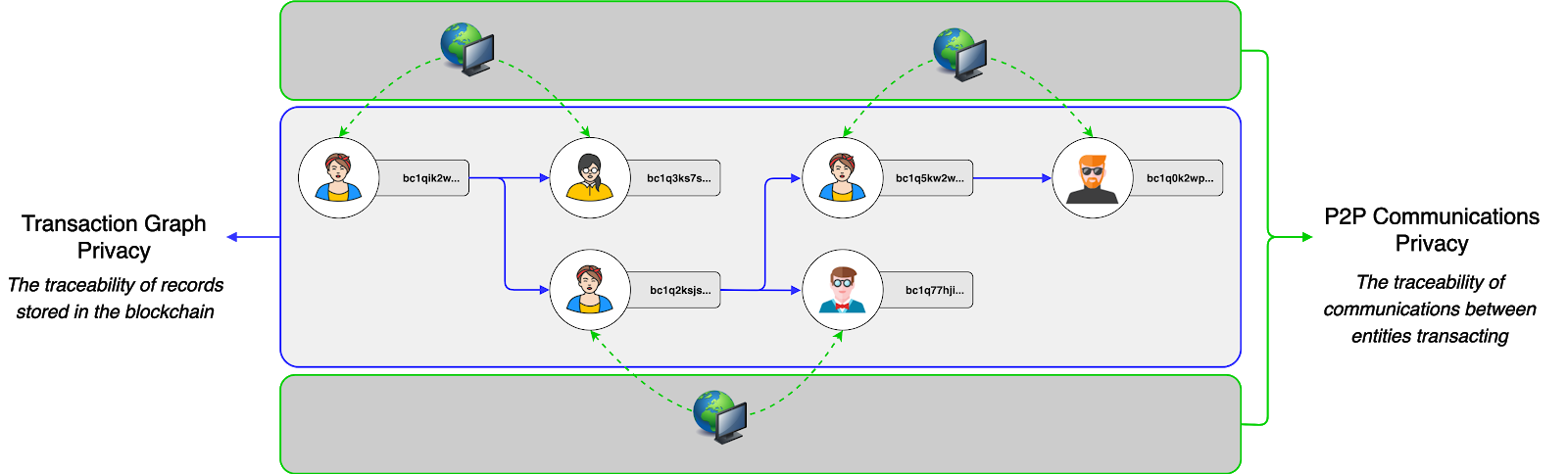

Before we delve into specific privacy innovations, it’s important to highlight that the biggest impediment to private transactions across digital assets is the fact that most solutions are half-baked. Privacy assets that focus on transaction-graph privacy often neglect network-level privacy, and vice versa. Both vectors suffer from a lack of maturity and usage, which makes transactions easier to de-anonymize via statistical traceability analysis at either the P2P network layer or the blockchain layer.

Thankfully, there are several projects pushing boundaries on both fronts.

Thankfully, there are several projects pushing boundaries on both fronts.

When it comes to transaction-graph privacy, solutions like P2EP and CheckTemplateVerify are interesting because privacy becomes a by-product of efficiency. As novel approaches to CoinJoin, these solutions can increase the adoption of private transactions by users that are solely motivated by lower transaction fees. Although privacy guarantees are still suboptimal under a CoinJoin model, unshielded sent amounts can still be beneficial, as they preserve the auditability of Bitcoin’s supply and free float.

If lower transaction fees become a motivator and lead to an increase in Bitcoin’s anonymity set (the % of UTXOs that are CoinJoin outputs), de-anonymization via statistical clustering analysis will become even more subjective than it already is. Some blockchain analysis companies have been able to trick law enforcement agencies into believing an assigned probability that a UTXO belongs to a specific user, but the underlying model is already extremely nuanced and fragile. If the majority of UTXOs become CoinJoin outputs, that might break existing approaches to clustering.

Before that can happen, there’s a tremendous amount of work that needs to be done on the usability front so that all Bitcoin users, tech savy or not, have equal access to privacy mechanisms. Beyond P2EP and CheckTemplateVerify, a recent development in usability was the proposal of SNICKER (Simple Non-Interactive CoinJoin with Keys for Encryption Reused), a novel way to generate CoinJoins with untrusted peers. SNICKER combines several technologies to grant users access to CoinJoin transactions without having to trust or interact with their peers.

Progress is also noticeable in protocols that aim to improve the privacy and efficiency of P2P communications. Over the course of 2019, the privacy-preserving network protocol Dandelion was successfully tested across multiple cryptonetworks. Even though privacy in transaction propagation is not a silver bullet when it comes to the full spectrum of P2P communication, protocols like Dandelion can still meaningfully increase user privacy by hiding the originating IP address of a nodes broadcasting a transaction.

A final development in Bitcoin’s networking stack worth highlighting is a new transaction relay protocol called Erlay. Although still at a very early development stage, Erlay is an important innovation because it can considerably reduce the bandwidth requirements of running a Bitcoin full node. If implemented, Erlay’s efficiency gains can enable users to participate in transaction relay, which is bandwidth intensive, and continuously validate the chain, especially in countries where Internet Service Providers impose caps on bandwidth.

The Tip of the Iceberg

It is incredibly difficult to track all the innovation happening in Bitcoin, and this post is just a scratch on the surface. This brings us to the key takeaway of this piece: Bitcoin, in its totality, is a constantly evolving suite of protocols. The modular approach to innovation described here is important, as it plays a key role in minimizing politicism in the evolution of Bitcoin and protects its fundamental monetary properties. Remember this article the next time someone claims Bitcoin is a static technology.

Connect with DAR

If you would like to learn more about DAR, click here to reach out. For our free daily newsletter chocked full of the highest quality crypto news and information, sign up here.

Bitcoin’s Missionaries vs Wall Street’s Mercenaries

By Anthony Pompliano

Posted December 3, 2019

This installment of Off The Chain is free for everyone. I send this email to our investors daily. If you would also like to receive it every morning, join the 38,000 other investors today.

To investors, There are a lot of common misconceptions surrounding Bitcoin. These usually revolve around cybersecurity, energy consumption, monetary competition, or some other nuanced element of the digital currency and the tertiary impact on the world. But one misconception is rarely spoken of — the difference between mercenaries and missionaries. This framework was developed by John Doerr, the famous venture capitalist who led Kleiner Perkins Caufield & Byers for many years, and was first presented publicly when he said “we need teams of missionaries, not teams of mercenaries.”

The Harvard Business Review did a great job explaining what Doerr meant by this in an April 2016 article:

As Doerr explained to an audience at Stanford Business School, mercenaries are “opportunistic.” They’re “all about the pitch and the deal” and are eager to sprint for short-term payoffs. Missionaries, on the other hand, are “strategic.” They’re all about “the big idea” and partnerships that last, and they understand that “this business of innovation is something that takes a long time” — it’s a marathon, not a sprint. Mercenaries have “a lust for making money,” while missionaries have “a lust for making meaning.” Mercenaries obsess about the competition and fret over “financial statements,” while missionaries obsess about customers and fret over “values statements.” Mercenaries display an attitude of entitlement and revel in the “aristocracy of the founders,” while missionaries exude an attitude of contribution and welcome good ideas wherever they originate. Mercenaries strive for success; missionaries aspire to “success and significance.”

John Doerr used the framework to talk about entrepreneurial teams, so what exactly does this have to do with Bitcoin and finance?

More than you would think. Generally, Wall Street is full of mercenaries. These individuals are focused on profits. They operate in a cutthroat environment where everyone in a deal is trying to screw over everyone else. Employees will leave in a heartbeat for bigger bonuses or more opportunity. There is very little loyalty and most people make decisions optimized around personal gain.

This is almost the complete opposite of the Bitcoin ecosystem. Rather than mercenaries, Bitcoin has benefited from a long list of missionaries. Whether it is Wences Casares teaching Silicon Valley luminaries one after the other about Bitcoin in the early days or Andreas Antonopoulos traveling around the world to educate millions of people for free, Bitcoiners believe in something much more important than profits. They believe in a better world. They see Bitcoin as a way to break the current systematic issues plaguing society. Simply, they believe that Bitcoin can change the world.

When mercenaries and missionaries compete with each other, the missionaries usually prevail. They believe in what they are doing on a much deeper level. They are willing to go to greater lengths to succeed. They can endure more pain. They refuse to give up. The mission is so important that the missionary is willing to dedicate their lives to seeing it come to fruition.

This fanaticism is what has driven Bitcoin from non-existence to one of the most popular currencies in the world in only one decade. People are drawn into the Bitcoin ecosystem for many reasons initially — some for profits, some for the technology, some for the polymath-like complexity — but almost anyone who stays around through the bull and bear market cycles has a belief in something much more important than profits.

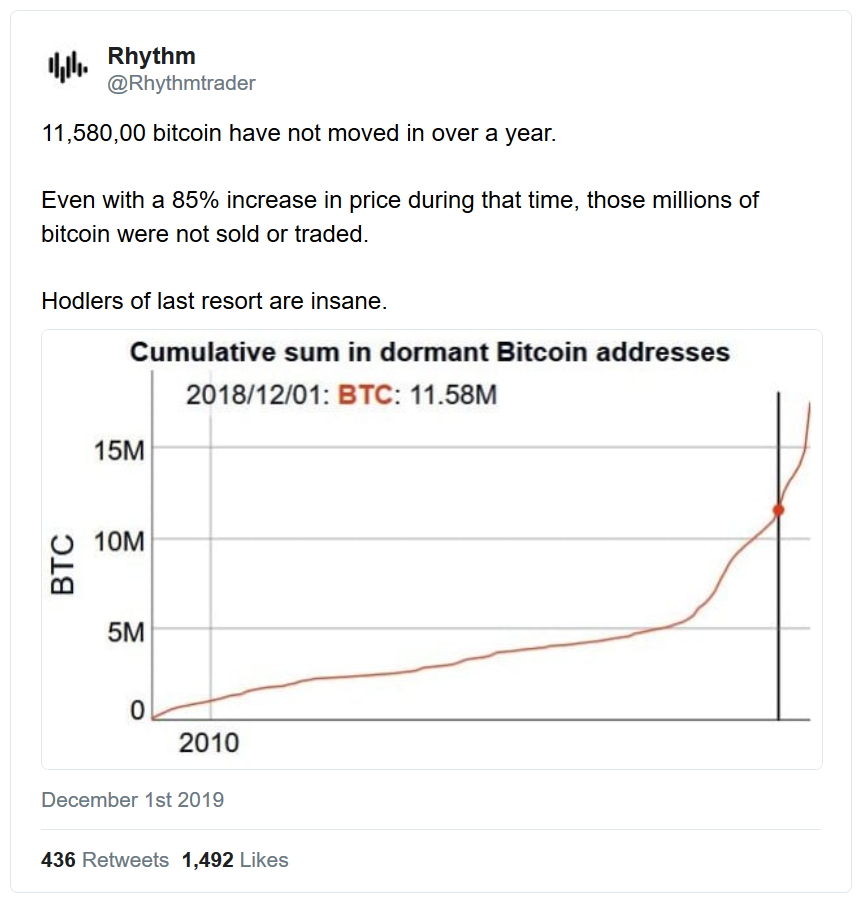

Nowhere is this more apparent than when we evaluate what people are doing with their Bitcoin. Twitter analyst @Rhythmtrader recently looked at how many people have moved their Bitcoin in the last year and found that more than 11,500,000 haven’t moved at all.

These people don’t care about the USD exchange value of Bitcoin. They believe in Bitcoin. They won’t be shaken out by price movements. In their mind, 1 BTC equals 1 BTC. We aren’t building a new trading asset, we are building a new financial system that decentralizes power from a corrupt and rigged system.

For Bitcoiners, this isn’t an investment. It is a protest. A peaceful protest against the system. Better yet, Bitcoin is a revolution. A revolution that stands to change the world in ways that most people can’t even comprehend yet. If successful, Bitcoin will usher in a new era where there is a separation of state and money. One where people are asked to trust transparent software systems over humans.

Quite literally, Bitcoin will disrupt the power structure of the world by simply surviving. For some, this is a scary world. For others, it is a necessary world.

And this is the largest misconception in the institutional investment world. The decision to allocate capital is not about today’s price and where it may go in the future. It is much more simple than that. Most institutional investors have 100% of their portfolio exposure in the dollar-denominated, fiat financial system.

There is now a new financial system being built. An alternative. Plan B. By choosing not to allocate any capital to this new financial system, institutional investors are claiming 100% confidence that the legacy system will survive. That the legacy system will prevail.

But if an institution thinks there is even a 1% chance that this new financial system will thrive, they must allocate capital to that system or risk missing one of the most disruptive events of our lifetime. The allocation percentages of the new and old system should mirror the confidence level that an institution has in each financial system winning over the long run.

But institutions aren’t missionaries. They are mercenaries. They play games of probability. They underwrite risk. They are unemotional about their investments. So we shouldn’t expect them to have more than 1-5% exposure to the new world.

But Bitcoiners are the exact opposite. Bitcoin isn’t risky to them, not owning Bitcoin is risky. These missionaries believe in something that seems irrational to most. But if Bitcoiners are successful, the mission will seem obvious in hindsight.

Whenever I see missionaries competing with mercenaries, the choice is obvious. And to say that I believe in the future potential of what we are all building would be an understatement. The current system is broken for most people. They can’t get ahead. They have no way to fight back. The issues are systemic. And there won’t be a solution until we change the system.

Bitcoin is doing just that. As Rhythmtrader said so eloquently, “Hodlers of last resort are insane.” But in the future, the nocoiners will be seen as having been the insane ones.

-Pomp

Tweetstorm: A Decade in Bitcoin

By Lucas Nuzzi

Posted December 5, 2019

2010 - Satoshi decentralizes Bitcoin by leaving his leadership role as its creator, and never again commenting on its development.

The Bitcoin community self-organizes, and begins to grow into new type of global institution.

2011 - The Silk Road showcases one of the biggest virtues of Bitcoin; it can’t be censored or confiscated. A drawback? It’s not private.

The Mt. Gox fiasco highlights infrastructural deficiencies; the lack of secure custody standards and the systemic risks imposed by exchanges.

2012 - BIP23 formalizes the concept of mining pools, an emerging structure that further decentralizes the power structures within Bitcoin.

BIP32 introduces HD keys & sets a new standard for Bitcoin custody and user onboarding via safer wallets.

2013 - BIP39 introduces mnemonic keys to Bitcoin.

➡️➡️For the first time in human history, you can store your wealth in your brain by memorizing 12 words. No centralized intermediaries needed. ⬅️⬅️

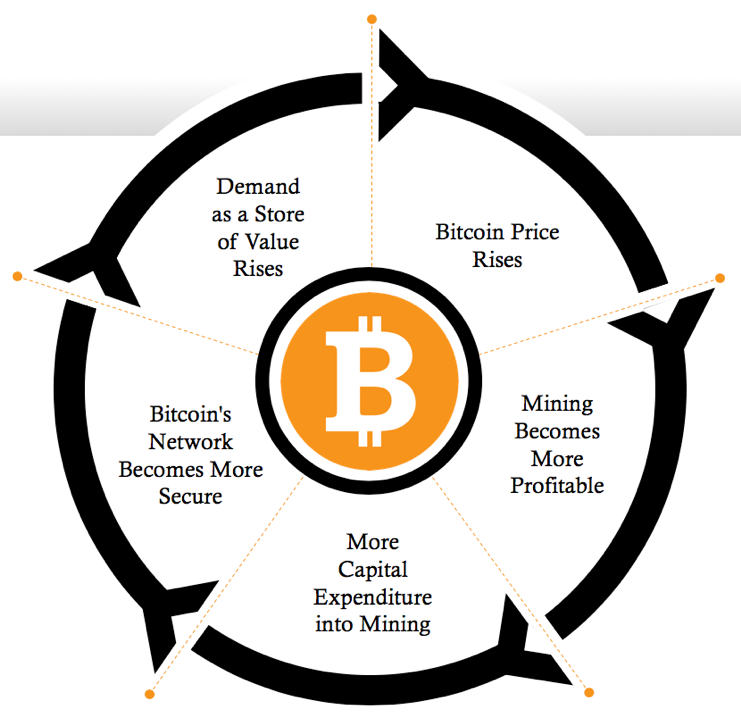

2014 - BIP42 makes it impossible for Bitcoin’s 21M cap to be infringed upon via continuous mining.

Mining industrializes and hashrate surpasses 100 PH/s for the first time.

Meanwhile, pundits claim Bitcoin is dead and that the future is “blockchain, the miraculous database”

2015 - On-chain volume hits an all time high and tensions are visible. The power structures in Bitcoin are tested with 9 competing block-size-increase BIPs.

We faced the question: Who controls Bitcoin?

Miners?❌ Developers?❌ Personalities? ❌ Users ✅

2016 - “The Bitcoin Lightning Network” is published.

As the risks of on-chain scaling become clear, promising alternatives like Lightning show that a layered, backwards-compatible approach to technological innovation is possible.

BIP114 introduces MAST and minds are blown. 🤯

2017 (a) - The global speculative bubble brings Bitcoin to the masses. Orange Bs can be seen everywhere.

Infrastructure is being pushed on all fronts; custody, markets, wallets, education.

Bitcoin becomes a liquid asset on a global scale. 🌎

2017 (b) - One of the most important events in Bitcoin history also takes place in ‘17: the SegWit2X fork.

There’s an attempt to highjack Bitcoin with plenty of enterprise support: the ultimate stress test of Bitcoin governance

USAF reinforces that users are the ones in charge

2018 - “Enterprise Blockchain” is now a sad meme.

The ecosystem outside of Bitcoin faces a series of hard realizations:

Scaling is hard, on-chain governance is flawed, deployment takes time, and you might have broken the law.

Institutions converge on BTC.

2019 - Bitcoin is now a movement with representatives everywhere; in media, government, traditional finance, tech. It’s like Fight Club, but rule #1 to only talk about it.

Bitcoin started this decade on the fringes.

We now have a bitcoiner in a US state senate.

Bitcoin had everything to die in multiple occasions over the course of this decade… it didn’t.

Its power structures were tested over and over again. Yet, here we are.

Who would’ve thought a leaderless system that converts electricity into money would’ve lasted this long?

As we approach a new decade of social anxieties, geopolitical tension and crazy monetary policy, you can be sure Bitcoin will still be here. There’s no way to put the genie back in the bottle.

I think Hal would’ve been proud. You too should start:

Ignorance about Bitcoin Disguised as Caution

By Rollo McFloogle

Posted December 7, 2019

Bitcoin has done a lot in its 11 years of existence. Perhaps one surprising role of Bitcoin has been exposing economic ignorance—namely the economics of money—of many people. I humbly include myself in that category of people (fortunately, it can also be an invaluable tool for helping you to learn the subject as well). Bitcoin is a nebulous and mysterious amalgam of technical computer science and economics to the newcomer. Very few people, even experts in one field or the other, can instantly grasp all that is Bitcoin. It takes even the best of minds some time to sort through and figure out.

We all can identify money. We use it a lot and think about it even more. It is absolutely instrumental in our ability to perform economic calculation, which is what we do when we use the information that prices provide to help us best direct resources to their most efficient uses. But while we can talk about any number of things about money, few people are actually able to explain what money truly is and how any given thing that is used as money came about.

This confusion is one of the things that pulls people into many incorrect conclusions about Bitcoin, including plenty of well-respected people. This includes, Jeffrey Tucker, who recently penned a piece on the American Institute of Economic Research (AIER) called “A Cautious Retrospective on Bitcoin.”

Tucker was an early enthusiastic proponent of Bitcoin, then got sucked into the Bitcoin Cash and altcoin hype, and now I’m not exactly sure how to categorize him.

In his AIER piece, Tucker lays out five reasons why he’s feeling a little bit more on the bearish side of Bitcoin and by doing so shows that he has some key misunderstandings of Bitcoin.

Let’s dive into his piece.

Before his list of five cautions, Tucker starts by showing two charts, one of transactions per day and the other of the USD exchange trade volume. He points out that transactions are at 2016 levels and exchange volumes are at 2017 levels. He then shows a third chart of wallet usage, which is steadily rising at an increasing rate, but that metric “belies the hope of a disintermediated money.”

Has Bitcoin taken a step backwards and is it on the decline? It’s ironic that Tucker, a man who like the rest of us scoffs at all the announcements that “Bitcoin is dead” during a bear market, would get so easily rattled in the latest lull following the by far biggest bull run to date. To be fair, he hasn’t bought the casket yet, but it is surprising that Tucker apparently believes that trading activity during a surge to almost $20,000 per bitcoin would sustain itself after the price correction. We all saw what was going on in late 2017. Everyone and their mother were trying to buy and sell Bitcoin. Once the price fell back down, did anyone really expect the people trying to get rich quickly to stay in the market?

Regardless of whether or not 2016 and 2017 were cherrypicked to compare metrics, Tucker’s problems are predicated from his idea that the health of Bitcoin’s adoption is based on how much it is transacted with. Since money’s primary use is as a medium of exchange, Tucker and many other critics of Bitcoin make the mistake of believing that money is only useful for spending in the present. They ignore that the delay of exchange, also known as saving, is also a perfectly valid—and not to mention absolutely critical—use of money. After all, what is money but a tool that transports current value across time and space for future uncertainty?

This describes money’s ability to function as a store of value, which as Michael Goldstein put it is “a metaphor for using a medium of exchange for exchange in the long term.” Bitcoin is still in its very early stages and those of us who see it as a way to shore up the attack surfaces that destroyed the gold standard believe that it will have a much greater value in the future as it monetizes around the world in the winner-take-all game of money. Meanwhile, fiat bolstered by legal tender laws is continuously inflated by central banks, pillaging the purchasing power of money. And we’ve seen the results of this: when money is expected to be worth less tomorrow than it is today, there is a strong incentive to get all the stuff you can exchange it for in the present. Everyone thinks about gratification today without regard for tomorrow. Prices are corrupted and economies have to absorb huge amounts of waste.

Thank goodness for sound money, the only medicine for this disease. When someone has both Bitcoin and fiat, he expects the value of the former to appreciate while he expects the latter to lose its value over time. Any rational economic actor will choose to spend his fiat while holding his Bitcoin whenever he can. This is Thiers’ law. He will also begin to demand payment in Bitcoin while charging a premium if someone must pay him in fiat. Eventually, everyone dumps their fiat on the greatest fools and it becomes so valueless that no one will accept it as payment even at great premiums. Since Bitcoin is now the only acceptable means of payment, it has become the common medium of exchange.

But since Tucker brought up numbers and charts as metrics for his proof that Bitcoin’s adoption is waning, let’s consider some of our own. It’s tough to point to a metric to show that people are using Bitcoin as a savings vehicle, but there certainly are things we can look at to check its health.

The first one is price in USD. Putting the y-axis on a logarithmic scale helps show the value appreciation of Bitcoin much more clearly.

Source: https://bitcoincharts.com/charts/bitstampUSD#tgMzm1g10zm2g25zl

Source: https://bitcoincharts.com/charts/bitstampUSD#tgMzm1g10zm2g25zl

What cannot be ignored is that while new bitcoins are being added to the supply through the mining process, if demand remained the same throughout this process, then the price would drop. Despite the local peaks and valleys, the overall trend of Bitcoin is a rising price, so demand must be increasing. Even if it’s only the current people in Bitcoin contributing to that demand, increases in price is a powerful signal to others that they should probably get in.

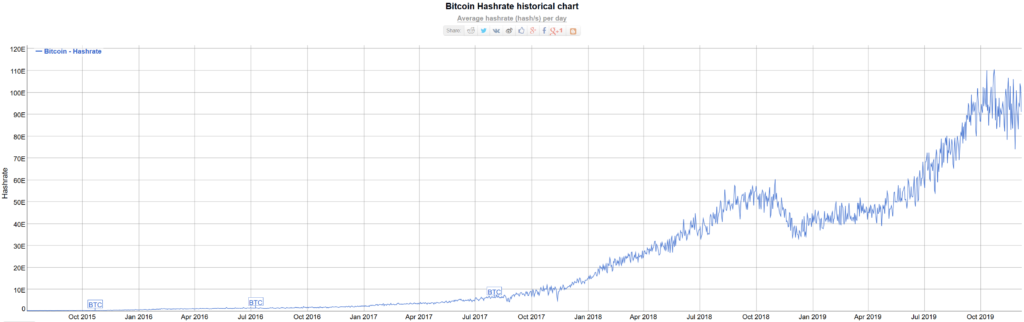

The other interesting metric to observe is Bitcoin’s hash rate, which is the number of hashes (guesses to solve a block) per second that the aggregate of miners makes across the network. In order to contribute hashes to the network, a miner must run software on specialized hardware. This hardware requires electricity, so mining Bitcoin with any chance of solving a block requires a significant commitment of expenditures for electricity. Miners want the block reward and transaction fees when they are the first to solve a block, so they’re careful not to break any rules (i.e. create an invalid block) that would cause all the validating nodes in the network to reject their block. If they submitted an invalid block, it would mean all the money they spent to solve it would be wasted, so miners tend to remain honest. This arrangement is what is referred to as “proof of work.” Using proof of work also means that any miner who wants to reverse transactions and rewrite history would have to spend enormous amounts of time and electricity to resolve previous blocks to submit a chain with the most proof of work to the network.

Miners add hash rate to increase their chances of solving a block and receiving the reward. More hash rate for the network means more proof of work, making it more expensive to attack, but it also makes it more difficult to solve blocks. Miners, being rational economic actors just like anyone else, are not interested in losing money on their operations.

*Source: https://bitinfocharts.com/comparison/bitcoin-hashrate.html

*Source: https://bitinfocharts.com/comparison/bitcoin-hashrate.html

The chart above shows that the hash rate is the highest it has ever been. If the overall value of Bitcoin were diminishing, then why would miners be spending so many resources on it? Certainly it could mean that miners are finding cheaper sources of electricity (they are), but that search for cheap electricity is a good signal that participation is in high demand since they must seek an advantage to stay competitive.

All of this shows that Tucker doesn’t have a good approach in either the economic or technical basics for viewing Bitcoin. This will help inform us to understand his perception of Bitcoin as we address each of his five considerations.

- Underpriced market assets are grounded in information asymmetries. Profits come from possessing valuable insight that others do not share, and acting on that insight. These asymmetries can be large or small. They were very large in Bitcoin from 2009 to 2015 or so. Some of us were convinced while vast numbers of even highly sophisticated people were sure that it could not, and the results were impressive for those who took the risk.

We are now eleven years into this, and the skeptics are now in a small minority. That blockchain technology is awesome is a given. If there were vast asymmetries in knowledge in the past, those have dissipated over time. The process of price discovery might have settled into a confident equilibrium: this stuff is cool, and useful for some purposes, but it cannot be a money for the world. It’s a given that there is no “true price” for Bitcoin but it is also true that the days of astonishment that it worked at all are now settling into the widespread awareness of why it works today.

With the full hindsight at our disposal, imagine being 11 or so years into the start of the internet and saying, “You know what, we’ve had the internet for awhile and plenty of people know about it, but it hasn’t been all that world changing, so I’m not sure this is really going to work out.” (We’re looking at you, Paul Krugman.) The success of the internet doesn’t guarantee the success of Bitcoin, but it does give us some insight on how global protocols take time to be fully implemented.

While much of the world’s population has had enough exposure to Bitcoin to at least know what it is, that doesn’t mean that knowledge about Bitcoin has settled equally among all these people. Knowing of and knowing about are two very different things. How many people simply aware of Bitcoin understand how it works or what its value proposition is? How many people even understand the economics of money well enough to act on the information they get about Bitcoin? How many people are aware of second layer solutions like the Lightning Network and sidechains that can massively scale Bitcoin?

These questions matter because money is for everyone. Everyone doesn’t need to know why or how it works (look at the internet again), but their ignorance about its usefulness explains why they’re not using it. And in fairness to these people, even if they weren’t too happy with the inflationary fiat system but didn’t worry much about censorship, they wouldn’t necessarily be drawn to use Bitcoin because the on-chain layer is not a superior substitute to the services they use for their day to day transactions in terms of cost and speed. Those who understand that the on-chain layer provides the security for the soundest money in the history of the world will compete for the bitcoins that are available for sale as they speculate that future layers built on top of this first layer will be the infrastructure that makes transitioning to Bitcoin the only play for even the ignorant.

- At the same time Bitcoin was launched, so too were released some other impressive payment technologies designed to reduce the price of transactions and make accepting credit cards vastly easier. Back in the day, small merchants had a very hard time accepting credit cards. Thanks to technologies like Square, even a lemonade stand can accept them using a smartphone, which was also launched around the same time. The near-universal use case for Bitcoin was once obvious; apart from specific demographics and interests, the case for broad public adoption is no longer clear. To be sure, there remain vast and important uses for crypto for permissionless remittances and for allowing the unbanked to move money (one of the booming facets of the crypto-asset sector are ATMs), but that will remain true regardless of market valuations.

It is truly a shame that Jeffrey Tucker puts censorship-resistant digital scarcity as a secondary value proposition for Bitcoin. Governments coopted central banks to use seigniorage to fund their massive expansions in size and scope, which has allowed them to wage endless warfare since. They removed the gold standard and constantly inflate the money supply, which further inflate bubbles of malinvestment. These bubbles, as part of the business cycle, have destroyed massive amounts of wealth and have prevented people from directing resources to their most efficient uses. Humanity is years behind in production and overall quality of life because governments can censor and create money on a whim. Bitcoin gives anyone with a computer and an internet connection the ability to remove the need for a trusted third party to send and receive money and to validate that the money they’re receiving isn’t counterfeit. This final settlement that once took large amounts of time and money now takes minutes and maybe a few dollars.

Bitcoin strikes at the root of the ability of governments to hold power. This innovation is world-changing. It is the zero-to-one event that can lead to a flourishing that humanity has never seen before. That was the hard part. Compared to that, it will be easy to build services for making fast and cheap payments on top of that.

- The old pitch for Bitcoin – that it made payments fast, cheap, and permissionless – had been dramatically changed as adoption increased and the portals couldn’t keep up. Permissionlessness still survives but that is not true of fast and cheap. By 2017 it became very obvious to the world that though Bitcoin is wonderful, it is not very practical for payments as compared with legacy systems that had vastly improved. Forks emerged to fix that problem but because the crypto sector is so vast, none could develop the network that Bitcoin obtained as the first mover in the space. Among those crypto innovations have been stable coins that operate as settlement banks. Those in the market for stability will find these more useful than old-fashioned crypto. And let us not forget the greatest lesson of monetary history: it’s the use value of a currency that is its value (there is no such thing as “storing” value).

Tucker, and many like him, first entered the Bitcoin space when some people were selling it as a fast and cheap payments processor. The reality, however, is that Bitcoin allows anyone to run a fast and cheap money validator. Consider what the last sound money system, the gold standard, involved. We tend to take for granted all the trust and centralization that had to occur simply for someone to use stamped gold coins. Imagine the cost—no wonder that work got entrusted for someone else to do. It is totally impractical for an individual accepting gold payments to test that the gold he is receiving is the gold that he is expecting for every single payment.

Bitcoin fixes this. Running a full node allows the user to trace any bitcoins that he is receiving all the way back to when they were first mined. This happens nearly instantly. Once the transaction is signed with a modest transaction fee, final settlement (the transfer of custody over the bitcoins) occurs in minutes (although your time depends on how many confirmations you want before you’re comfortable).

Bitcoin was the first mover in the space, but that’s not the reason it dominates its industry. It is by far the most secure in its ability to provide final settlement and maintain its monetary properties. Altcoin competitors are often centralized and at best only offer a small fraction of the security provided by Bitcoin’s network of nodes and proof of work. It is the most liquid out of all the cryptocurrencies and will continue to gain in liquidity and market share as its competitors of all kinds approach values of zero. So-called stablecoins pegged to the dollar don’t solve any of the problems that Bitcoin sets out to and will be absorbed by Bitcoin’s dominance just like all the others.

- Bitcoin came into a banking world that was dilapidated and anachronistic. But banks and processors felt the heat and adapted in an unusually quick period of time. Now we have peer-to-peer payment systems working within the regular banking systems. We have Venmo, Zelle, Apple, and Google, and many other systems, and, for all their limitations, they are getting better by the day. For that matter, the Fed itself has announced its own plans for a blockchain-like P2P payment system. Competition works. Bitcoin made a major contribution to lighting a fire under the mainstream industry. But that innovation necessarily affects Bitcoin’s prospects.

Services like Venmo, Zelle, etc. may be nice because they add a layer for transferring money that is fast and cheap, but they are still controlled by gatekeepers who are at the mercy of the governments that operate where they are located. They offer no censorship resistance and do nothing to harden the money they’re built on top of.

Let the Fed make their own “blockchain-like P2P” payment system. I am astonished that Tucker found it at all interesting to mention them as competition against Bitcoin.

- Let’s just say – as many industry experts say to me in private – that the days of endless price increases of Bitcoin are over, and that it settles into a stable price and even gradually falls to 2014 or 2013 levels. That is not beyond the realm of possibility. Nothing about markets are perfectly predictable, and there is nothing baked into the nature of Bitcoin that guarantees any particular future. A major problem hits the essence of money itself: the use case is everything and adoption is the path toward making any money mainstream. The trends here do not look brilliant for Bitcoin.

Ah, the “experts” are saying that Bitcoin won’t see increases in price against the dollar. And while Tucker correctly points out that markets are not perfectly predictable, economics tell us that the hardest money wins. Can events happen in the future that prevent Bitcoin from fully monetizing? Of course, they can, but nothing Tucker has said in his article has convinced me to step back from my bullishness.

Tucker ends the piece by taking an agnostic stance on the future of money although he seems fairly confident that Bitcoin will flourish in the immediate future “to service a special type of need.” He leaves the possibility for anything to happen, from Bitcoin going “to the moon” to “something else entirely—an Amazon coin, for example.” He just wants people to have some humility in the process.

Humility is a good trait to have, but let’s not mistake a bearish outlook on Bitcoin because of ignorance as humility. Tucker’s suggestion of a completely centralized “Amazon coin” demonstrates his failure to understand the ultimate purpose of Bitcoin. The sun may not rise tomorrow. Am I being humble for not being so sure that it will? Obviously, the future of Bitcoin is harder to predict than the rising and setting of the sun, but you should see the point of my hyperbole. Bitcoin is on its path and it doesn’t care what either Jeffrey Tucker or I say about it. But Bitcoin is not cold and vengeful. It’s chugging along, happy to welcome anyone, no matter who they are, to its network. I look forward to the day when Jeffrey Tucker welcomes Bitcoin back.

Cryptocurrency Is Most Useful for Breaking Laws and Social Constructs

By Jill Carlson

Posted December 10, 2019

This post is part of CoinDesk’s 2019 Year in Review, a collection of 100 op-eds, interviews and takes on the state of blockchain and the world.

Jill Carlson is co-founder of the Open Money Initiative, a non-profit research organization working to guarantee the right to a free and open financial system, and co-host of the What Grinds My Gears podcast. She also works as an advisor and consultant for startups including Algorand, Risk Labs, dYdX, CoinList, and Tezos.

Why hasn’t cryptocurrency gone mainstream?

“It doesn’t scale.”

“It’s slow.”

“It’s expensive.”

“It’s volatile.”

“It’s hard to use.”

Or maybe it was never supposed to go mainstream.

This is not to say cryptocurrency is any less important, meaningful, or useful. Rather, I think perhaps we have been judging cryptocurrencies’ success (or lack thereof) according to a false metric. We would not judge a fish by its ability to climb a tree.

By design, cryptocurrency does not solve mainstream problems.

Scale, speed, and cost are all examples of mainstream problems within finance, from main street to Wall Street. Credit card networks go down. Stock trades take days to clear. Wire transfers are expensive. In some situations, cryptocurrencies may offer marginal improvements on any of these issues, but more often blockchain-based systems will fail when compared to more conventional, centralized solutions.

This does not represent a design flaw. In fact, this is an intentional trade off. Decentralized systems forsake scale, speed, and cost in favor of one key feature: censorship resistance. Cryptocurrency solves problems faced by the censored who, by definition, are not the mainstream.

In particular, cryptocurrency enables individuals and organizations to make censored transactions. Procuring drugs on the internet. That’s an example of a censored transaction. Buying US dollars in Argentina is another example. Paying a sex worker. Sending money to a friend in Iran. Making an online purchase as an unbanked individual. Selling cannabis as a dispensary. Getting money out of Venezuela. Supporting dissidents in Hong Kong. The primary utility of cryptocurrency lies in engaging in financial activity that is otherwise suppressed or prohibited.

This is the stated intent of cryptocurrency. Satoshi Nakamoto, the creator of bitcoin, described cryptocurrency as a tool of freedom. He compared it to other peer to peer networks like Tor which are similarly resilient to censorship. If we look at the anecdotal evidence, we can see that this is indeed how bitcoin is being used from China to Palestine. Furthermore, what little quantitative data we have also suggests that cryptocurrency use is higher in countries with financial restrictions. These results line up with predictions around cryptocurrency adoption that have existed for years. It is time to face this potentially uncomfortable reality: cryptocurrency is most useful when breaking laws and social constructs.

I, FOR ONE, DO NOT WANT TO LIVE IN A WORLD WHERE CRYPTOCURRENCY HAS FOUND MAINSTREAM USE.

There exists a long history of censorship resistant and privacy preserving technologies: Signal for messaging, Bittorrent for file-sharing, Tor for web browsing. Like bitcoin, these tools are not built for the mainstream. Most people would rather use faster, slicker, glossier centralized alternatives like Facebook Message, Dropbox, and Google Chrome. But for censored people and organizations, decentralized technologies have always provided an escape hatch. For as long as they have existed, these tools have brought with them a certain level of societal discomfort. This discomfort stems not from these platforms being lawless domains – regulations exist on the dark web as much as they do in any jurisdiction – but rather from the difficulty these platforms present in enforcing these government policies and social norms. These technologies render censored activities more difficult to stop.

Decentralized technologies can be used for good, for evil, and for everything in between. From Hammurabi’s Code through to the Patriot Act, the morality of laws has been a matter of debate for as long as they have existed. The laws of one jurisdiction are often deemed unethical and unacceptable by its citizens and those of other geographies. To say that cryptocurrency is used primarily to engage in illegal or socially unacceptable activities is not a normative statement. It is used by freedom fighters and terrorists, by journalists and dissidents, by scammers and black market dealers, by revolutionaries and government officials. It is used by civilians to break unjust laws and escape humanitarian crisis, and it is used by the policymakers who write those very same laws. And of course, the same statements can all be made regarding the original decentralized payment system: cash.

As an industry, we spend a lot of time considering how to drive mainstream adoption of cryptocurrency. I, for one, do not want to live in a world where cryptocurrency has found mainstream use. For if it has, that world is a very scary place indeed.